At a recent industry event, conversation turned – as it always seems to these days – to the economics of the AI buildout. It’s no secret that the AI race has involved massive and escalating capital investments in datacenters and other infrastructure, hardware, power and related cost centers.

For most of the conversation’s participants, however, it had been some time since anyone – us included – had examined the numbers in detail, both for the slope of the trajectory and for the context around the spending itself.

While any analysis of this type is limited by the data that’s available – large important players like Anthropic and OpenAI for example are, for now, private companies and therefore don’t report their metrics publicly – it is nevertheless worth looking at the investments large cloud players have made in recent years, and how they might compare to non-infrastructure centric technology vendors like Apple.

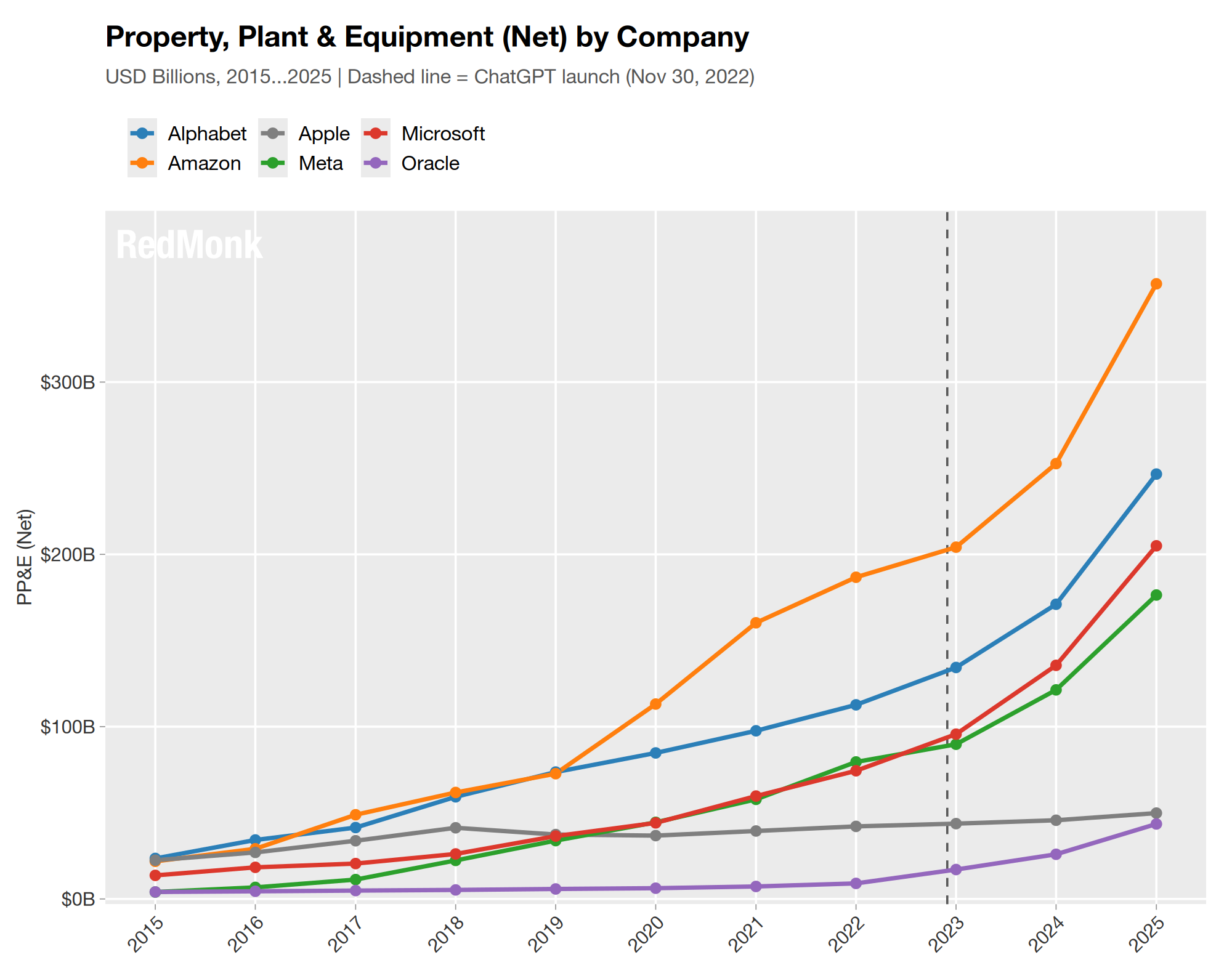

For starters, then, here is the Plants, Property and Equipment (PP&E) spend for the selected vendors over the past decade. As a side note, these PP&E figures exclude operating lease right-of-use (ROU) assets because the point of interest here is actual capital build out.

Of note here are the relative rankings in PP&E spend of the investments, as well as the slope pre- and post-ChatGPT release. Additionally, as has been well documented elsewhere, Apple has not felt compelled to respond to this cycle’s frenzied wave of datacenter construction and its PP&E spend has remained static while that of its industry peers has soared.

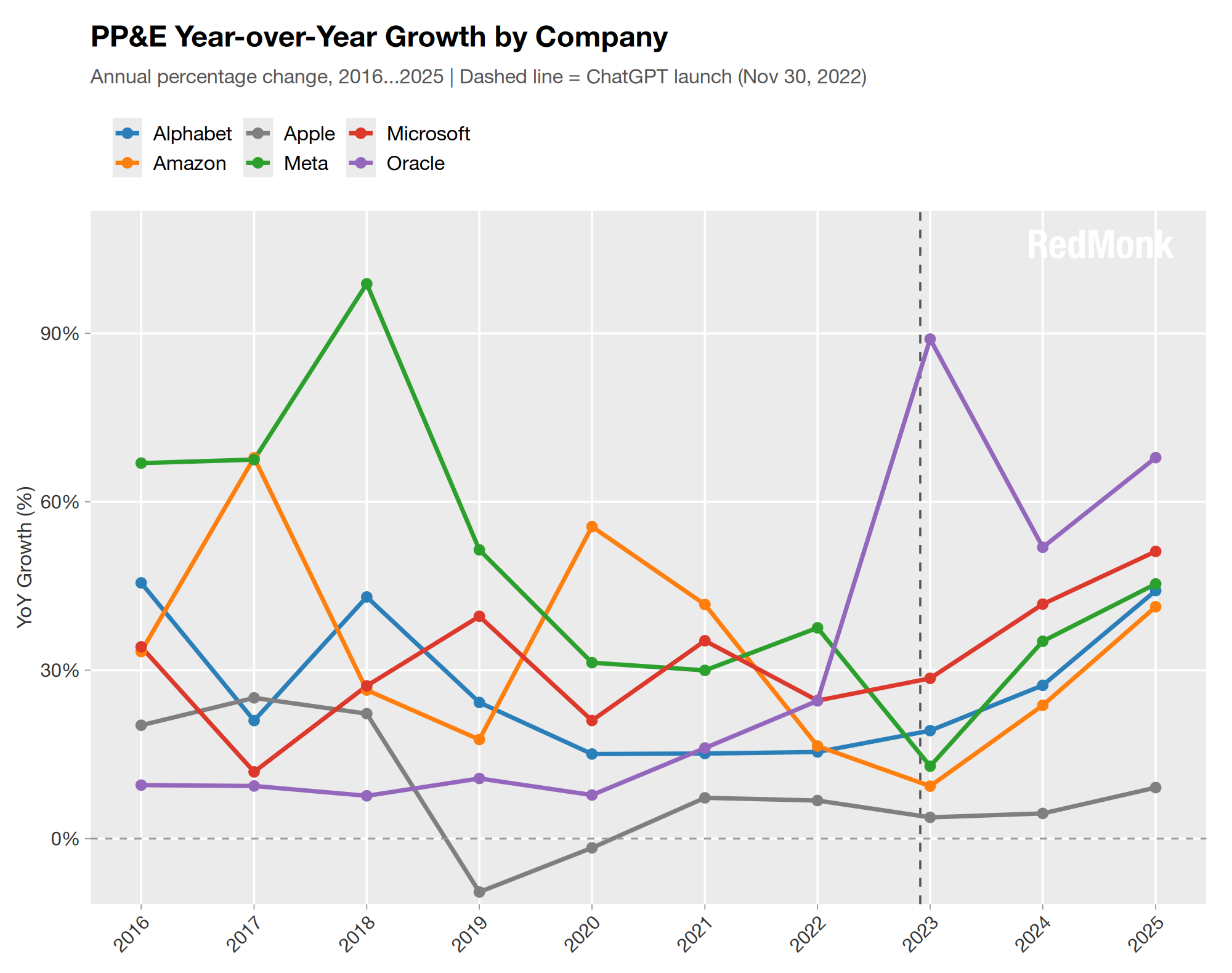

Next, here’s a look at the changes in PP&E spend per company year on year.

The most important note here is to ignore the 2023 spike in Oracle’s PP&E; that’s an artifact of its 2022 $28B acquisition of the electronic health records company Cerner, with its datacenter, infrastructure and facilities hitting Oracle’s books in the following calendar year.

Other than random spikes in investments from Amazon, Meta and others, the only significant takeaway from this chart are the slopes again pre- and post-ChatGPT. Year on year growth in PP&E spend had plateaued and arguably declined heading into 2022, which is appropriate as the cloud market was maturing six years in. But these trends took an about face in the wake of ChatGPT’s breakout success, and increases in PP&E spend immediately accelerated.

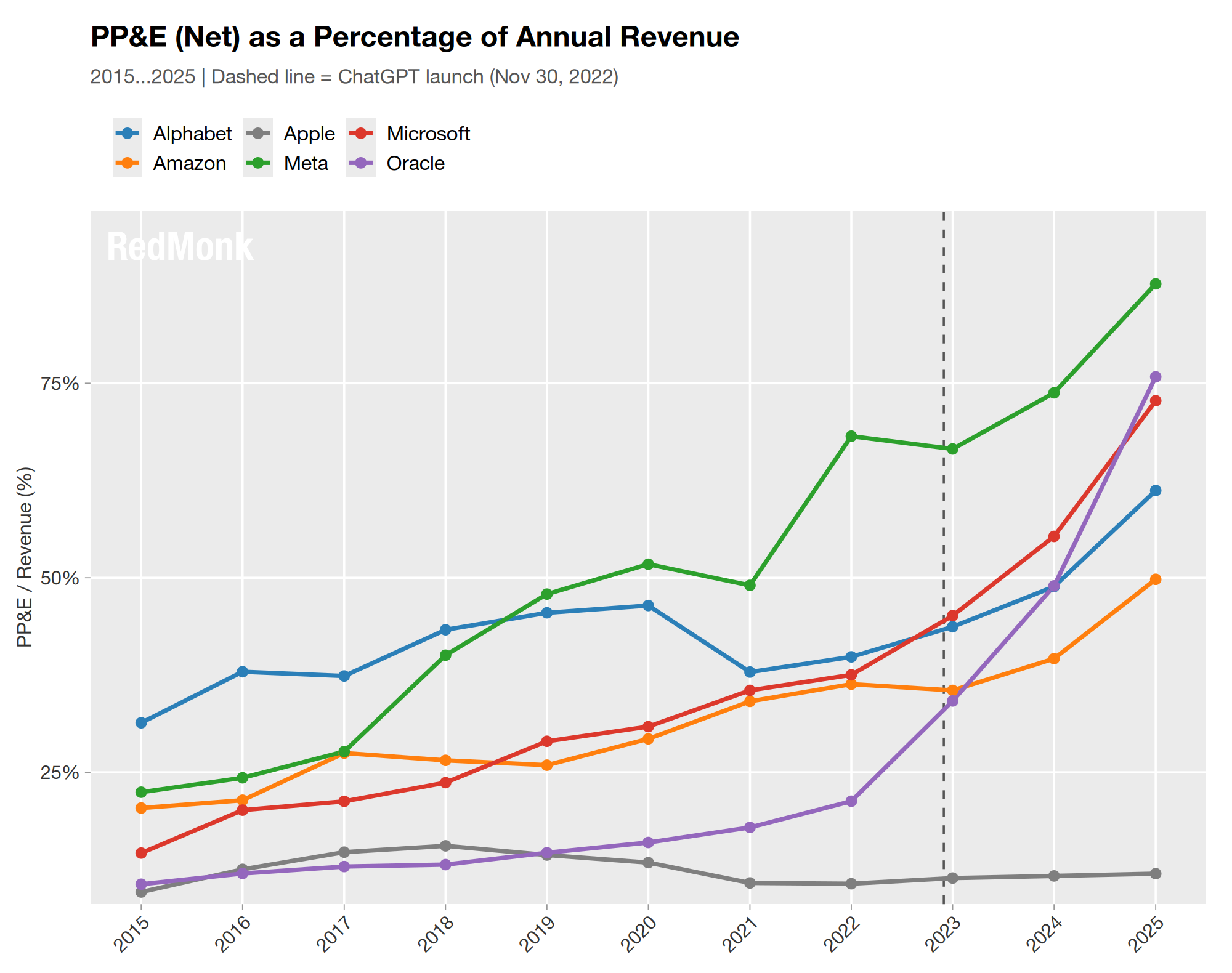

Arguably the most startling chart, however, is that of PP&E spend as a percentage of annual revenue.

Apple and Meta bookend this chart as the opposite ends of the spending spectrum. But it’s notable how close the trajectories of Amazon and Google, and later Microsoft and much later, Oracle are as a percentage of revenue. It is eye opening that all but one of these companies – Apple being the notable exception – are spending at least half of their revenue figure, and most well north of that, on new infrastructure.

That level of investment would have been unthinkable a decade ago. Today, the chart suggests it’s table stakes unless you’re a commercial device retailer.

While PP&E spend is too blunt an instrument to perform a much more detailed analysis, it both points to the extreme level of investment required to be regarded as a credible player and raises significant questions about where, when and how the return on these outsized investments will arrive.

Disclosure: Amazon, Google, Microsoft and Oracle are RedMonk customers. Apple and Meta are not currently customers.