Donnie Berkholz's Story of Data

Making sense out of information

-

The end of this story

-

React and Polymer arising among JavaScript MV* frameworks

-

Are we nearing peak language fragmentation?

-

RedMonk’s analytical foundations, part 4: 2011–present

-

RedMonk’s analytical foundations, part 3: 2008–2010

-

The breakout of Ansible, and the state of config-management communities

-

The emergence of Spark

-

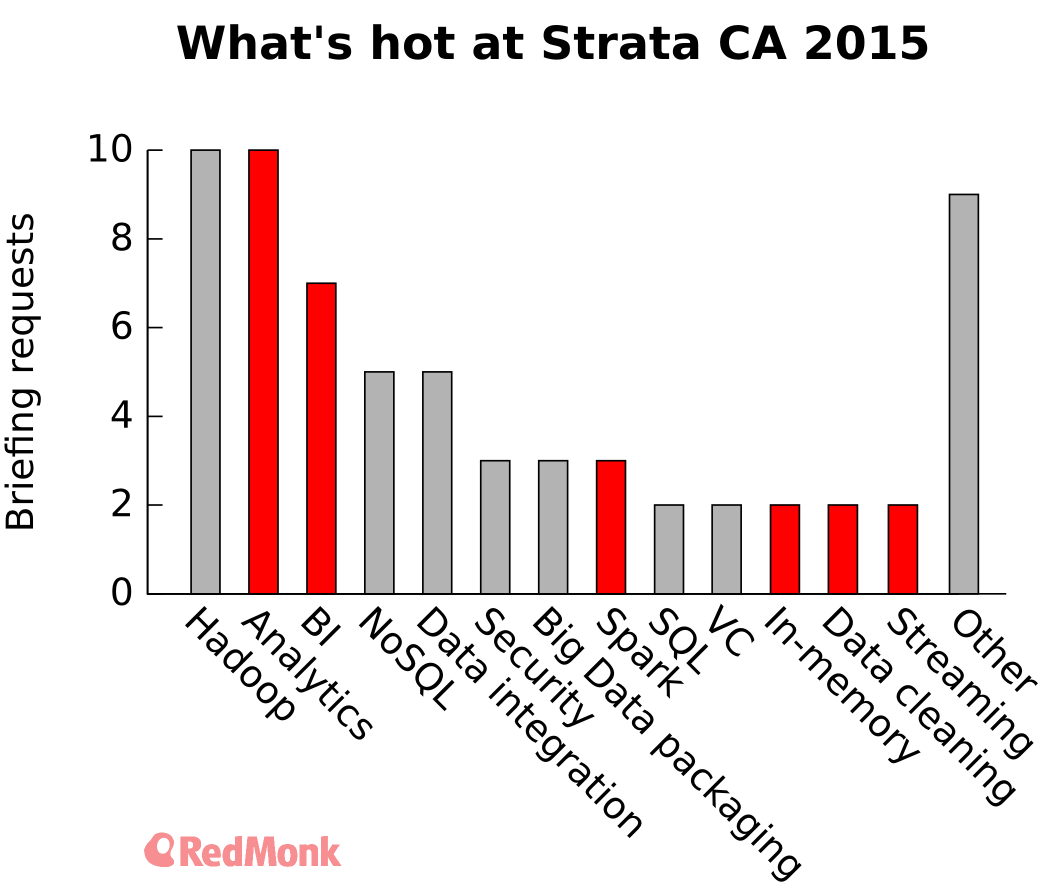

Strata 2015: Reaching for the business user

-

Cloud outages, transparency, and trust

-

Time for sysadmins to learn data science

-

Enterprise tech: the still-hot old thing

-

Docker, Rocket, and bulls in a china shop

Sponsor

Recent Comments