Even by the standards here, these 2014 predictions are late. But feeling that late is better than never, let the following serve as my official forecast for the year – or what’s left of it – ahead. As always, these predictions are based off of the information at hand, which in some cases might be quantitative forecasts and in others little more than rumor and speculation. The common thread, for me, is the belief that each will occur. Historically at RedMonk, we are better at predicting developments than their timing, and these predictions are no exception. Nevertheless, the following predictions are made for the year 2014.

One new wrinkle this year, as suggested by Bryan Cantrill, is the introduction of categories. In years past, all predictions have been issued as if they were of equal probability. The fact is, however, that not all predictions are created equal: some are more probable than others. To that end I’ve grouped this year’s predictions into five sections, ranging from very likely to theoretically possible. This will help when evaluting the predictions, because it will reveal the relative substance behind them.

With that said, on to the predictions.

Safe

-

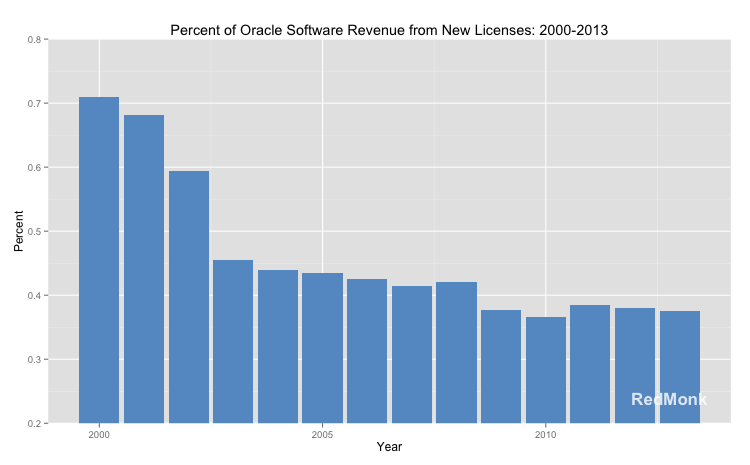

38% or Less of Oracle’s Software Revenue Will Come from New Licenses

As discussed in November of 2013 and July of 2012, while Oracle has consistently demonstrated an ability to grow its software related revenues the percentage of same derived from the sale of new licenses has been in decline for over a decade.

Down to 38% in 2013 from 71% in 2000, there are no obvious indications that 2014 will buck this trend.

-

The Biggest Problem w/ IoT in 2014 Won’t Be Security But Compatibility

All signs indicate that 2014 is likely to be a big year for the Internet of Things. From large scale M&A activity to conference traction, interest in network-attached devices is spiking. There’s seemingly a new Kickstarter every day for some new IoT project, and even traditional companies are moving into the space more aggressively. There are two big problems, however, looming. The first is security. Bruce Schneier, as always, deconstructs the issues here clearly in this piece from Wired. He is entirely correct: there is a reckoning on the horizon with respect to IoT devices, and just as was the case with PC security it’s going to get worse before it gets better. And the damage from compromised hardware is likely to be far greater; what if attackers were able to turn off tens of thousands of thermostats during freezing temperatures?My bet is that the second problem, however, is the more acute in the year ahead. Specifically, compatibility. Part of the promise of IoT devices is that they can talk to each other, and operate more efficiently and intelligently by collaborating. And there are instances already where this is the case: the Nest Protect smoke alarm, for example, can shut off a furnace in case of fire through the Nest thermostat. But the salient detail in that example is the fact that both devices come from the same manufacturer. Thus far, most of the IoT devices being shipped are designed as individual silos of information. So much so, in fact, that an entirely new class of hardware – hubs – has been created to try and centrally manage and control the various devices, which have not been designed to work together. But while hubs can smooth out the rough edges of IoT adoption, they are more band-aid than solution.

And because this may benefit market leaders like Nest – customers have a choice between buying other home automation devices that can’t talk to their Nest infrastructure or waiting for Nest to produce ones that do – the market will be subject to inertial effects. Efforts like the AllSeen Alliance are a step in the right direction, but in 2014 would-be IoT customers will be substantially challenged and held back by device to device incompatibility.

-

Windows 7 Will Be Microsoft’s Most Formidable Competitor

The good news for Microsoft is that Windows 7 adoption is strong, with more than twice the share of Windows XP, the next most popular operating system according to Statcounter. The bad news for Microsoft is that Windows 7 adoption is strong.

With even Microsoft advocates characterizing Windows 8 as a “mess,” Microsoft has some difficult choices to make moving forward. Even setting aside the fact that mobile platforms are actively eroding the PC’s relevance, what can or should Microsoft tell its developers? Embrace the design guidelines of Windows 8, which the market has actively selected against? Or stick with Windows 7, which is widely adopted but not representative of the direction that Microsoft wants to head? In short, then, the biggest problem Microsoft will face in evangelizing Windows 8 is Windows 7.

-

The Low End Premium Server Business is Toast

Simply consider what’s happened over the last 12 months. IBM spun off its x86 server business to Lenovo, at a substantial discount from the original asking price if reports are correct. Dell was forced to go private. And HP, according to reports, is about to begin charging customers for firmware updates. Whether the wasteland that is the commodity server business is more the result of defections to the public cloud or big growth from ODMs is ultimately irrelevant: the fact is that the general purpose low end server market is doomed. This prediction would seem to logically dictate decommitments to low end server lines from other businesses besides IBM, but the bet here is that emotions win out and neither Dell nor HP is willing to cut that particular cord – and Lenovo is obviously committed.

Likely

-

2014 Will See One or More OpenStack Entities Acquired

Belatedly recognizing that the cloud represents a clear and present danger to their businesses, incumbent systems providers will increasingly double down on OpenStack as their response. Most already have some commitment to the platform, but increasing pressure from public cloud providers (primarily Amazon) as well as proprietary alternatives (primarily VMware) will force more substantial responses, the most logical manifestation of which is M&A activity. Vendors with specialized OpenStack expertise will be in demand as providers attempt to “out-cloud” one another on the basis of claimed expertise. -

The Line Between Venture Capitalist and Consultant Will Continue to Blur

We’ve already seen this to some extent, with Hilary Mason’s departure to Accel and Adrian Cockcroft’s move to Battery Ventures. This will continue in large part because it can represent a win for both parties. VC shops, increasingly in search of a means of differentiation, will seek to provide it with high visibility talent on staff and available in a quasi-consultative capacity. And for the talent, it’s an opportunity to play the field to a certain extent, applying their abilities to a wider range of businesses rather than strictly focusing on one. Like EIR roles, they may not be long term, permanent positions: the most likely outcome, in fact, is for talent to eventually find a home at a portfolio company, much as Marten Mickos once did at Eucalyptus from Benchmark. But in the short term, these marriages are potentially a boon to both parties and we’ll see VCs emerge as a first tier destination for high quality talent. -

Netflix’s Cloud Assets Will Be Packaged and Create an Ecosystem Like Hadoop Before Them

My colleague has been arguing for the packaging of Netflix’s cloud assets since November of 2012, and to some extent this is already occurring – we spoke to a French ISV in the wake of Amazon reInvent that is doing just this. But the packaging effort will accelerate in 2014, as would-be cloud consumers increasingly realize that there is more to operating in the cloud than basic compute/network/storage functionality. From Asgard to Chaos Monkey, vendors are increasingly going to package, resell and support the Netflix stack much as communities have sprung up around Cassandra, Hadoop and other projects developed by companies not in the business of selling software. To give myself a small out here, however, I don’t expect much from the ecosystem space in 2014 – that will only come over time.

Possible

-

Disruption Finally Comes to Storage and Networking in 2014

While it’s infrequently discussed, networking and storage have proven to be largely immune from the aggressive commoditization that has consumed first major software businesses and then low end server hardware. They have not been totally immune, of course, but by and large both networking and storage have been relatively insulated against the corrosive impact of open source software – in spite of the best efforts of some upstart competitors.This will begin to change in 2014. In November, for example, Facebook’s VP of hardware design disclosed that they were very close to developing open source top-of-rack switches. That open source would eventually come for both the largely proprietary networking and storage providers was always inevitable; the question was timing. We are beginning to finally seen signs that one or both will be disrupted in the current year, whether its through collective efforts like the Open Compute Project or simply clever repackaging of existing technologies – an outcome that seems more likely in storage than networking.

To get an idea of what the impact of these disruptions might be, it’s worth considering Cisco’s own (reported) evaluation of what would happen if the networking giant aggressively embraced SDN: “They concluded it would turn Cisco’s ‘$43 billion business into a $22 billion business.'” The stakes are high, in other words.

Exciting

-

The Most Exciting Infrastructure Technology of 2014 Will Not Be Produced by a Company That Sells Technology

More and more today the most interesting new technologies are being developed not by companies that make money from software – one reason that traditional definitions of “technology company” are unhelpful – but from those that make money with software. Think Facebook, Google, Netflix or Twitter. It’s not that technology vendors are incapable of innovating: there are any number of materially interesting products that have been developed for purposes of sale.But if necessity is the mother of invention, few to none have the necessity that the web scale companies do.

-

Google Will Buy NestGoogle Will Move Towards Being a Hardware Company

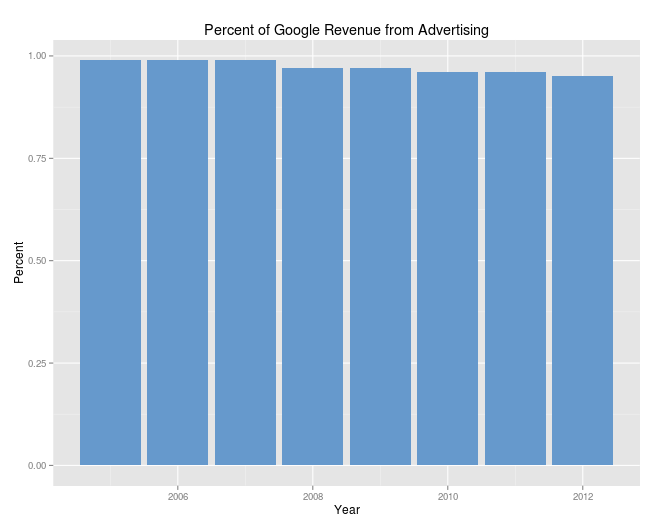

In the wake of Google’s acquisition of Nest, which I cannot claim with a straight face that I would have predicted, this prediction probably would have been better positioned in the Safe or Likely categories, as it seemed to indicate a clear validation of this assertion. But then they went and sold Motorola to Lenovo, effectively de-committing from the handset business.While Google’s true motivations in that sale are a matter of speculation, however, the fact is that Google is still on its way to becoming a hardware company. Not necessarily in revenue, at least in the short term, although revenue is part of the argument. Consider the following chart.

This is why people think of Google as an advertising company: because it is – at least from a revenue standpoint. The overwhelming majority of its revenues has historically, and does at present, come from ads. Slightly less each year, it’s true, but even today 95% of Google’s revenue is ad revenue. Not products, not services, ads.

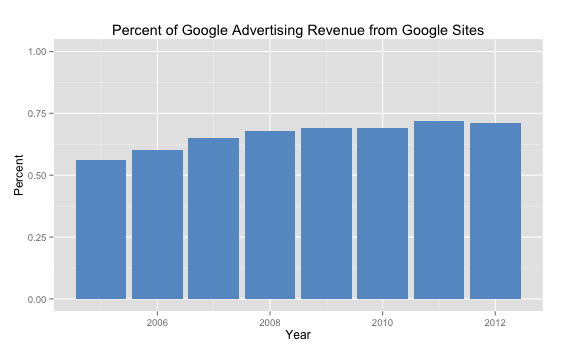

But within the ad revenue numbers, there’s an interesting trend that ought to concern Google.

In 2005, almost $0.50 of every advertising dollar Google earned came from non-Google network sites. By 2012, that number was down to $0.29. By itself, this isn’t a problem. Because Google’s network has grown substantially over that seven year span, it’s understandable that a higher percentage of advertising revenue would come from it. This is, essentially, the model that Android, Google Fiber and so on are built on. But Google has always had to hedge against an increasingly fragmented online world. Android is one such, but Google’s M&A behavior indicates that hardware will play a bigger role than many expect. Nest is what everyone remembers when they think of Google and hardware, both because of the valuation and the high visibility of its flagship product. But Google’s got more hardware plays, Motorola or no Motorola: Glass, self-driving cars, Boston Dynamics’ robots and so on. And speaking of Motorola, not many people noticed, but Google kept their Advanced Technology and Products unit during the Lenovo transaction.

What exactly Google plans to do with all of this hardware talent is as yet unclear, but it wouldn’t be a surprise to see Google begin making more substantial forays into the home, as the apparently mothballed Android@Home initiative was intended to do. Having first colonized the browser experience and then the handset, the home – and the car – are logical next steps. So while I don’t expect hardware to show up in the balance sheet in a meaningful way in 2014, it seems probable that by the end of the year we’ll be more inclined to think of Google as a hardware company than we do today.

Possibly related: what is Google doing with Hangar One?

Spectacular

-

Google Will Acquire IFTTT

Acquisitions are always difficult to predict, because of the number of variables involved. But let’s say, for the sake of argument, that you a) buy the prediction that a major problem with the IoT is compatibility and b) that you believe Google’s becoming more of a hardware company broadly and IoT company over time: what’s the logical next step if you’re Google? Maybe you contemplate the acquisition of a Belkin or similar, but more likely you (correctly) decide the company has quite enough to digest at the moment in the way of hardware acquisitions. But what about IFTTT?By more closely marrying the service to their collaboration tools, Google could a) differentiate same, b) begin acclimating consumers to IoT-style interconnectivity, and c) begin generating even more data about consumer habits to feed their existing (and primary) revenue stream, advertising.

Consider the mobile implications more specifically. Let’s assume, as Ben Thompson does – I believe correctly – that the viable business models in mobile are a) devices and b) services. Google has made clear which of those it will bet on, whether it was the sale of Motorola, the increasing distance between AOSP and the Google services behind it, or comments like these. Google’s existing services are solid, and market leading in some categories. But IFTTT offers the ability to extend these services and combine them with others in interesting, creative ways – particularly when Nest is factored in as well.

How the market would react is another question – at least anecdotally, the blowback from the Nest pickup appeared to be severe – but on paper at least IFTTT would be a very interesting complement to Google’s consumer services play, and just as importantly, one capable of feeding its still-advertising based bottom line.

Greg Knieriemen says:

February 17, 2014 at 11:50 am

Great predictions. Quick thoughts…

Commoditization of servers did not come about because of open source projects, it came from proprietary server virtualization.

Likewise to storage, I don’t think open source will impact storage commoditization… it will be storage virtualization. Storage virtualization has been available for about a decade but only recently has the largest storage vendor, EMC, discovered it. Before they called it “Frankenstorage” – now they call it “Software Defined Storage”.