"Our business is 99% selling SW & 1% hosted Cloud Foundry. It's an evolution of the whole middleware market." @wattersjames via @infoworld

— Pivotal (@gopivotal) March 11, 2014

As announced yesterday at their inaugural analyst conference, Cloudera – the first commercial backer of the Hadoop project – has secured $160 million in new financing, bringing their total raised capital to $300 million. Because it remains, at least for now, a private company, precise details on their finances remain unavailable. What has been disclosed, however, is that approximately seventy percent of their revenue derives from what the company refers to as “software.” The question that no one seems to be asking today is what the word “software” actually means in this context.

Twenty years ago, the logistics of software businesses were straightforward. Vendors employed developers, though they were systemically undervalued at the time, to collectively author a product that was explicitly designed to be sold to a specific buyer. By the late 1980’s in the case of the enterprise, this was typically the Chief Information Officer. While software was virtual by nature it was typically distributed in physical form, whether that was a floppy disk, a CD-ROM or, later, a DVD. Software businesses, in other words, looked a great deal like traditional manufacturing businesses: they constructed a product, shipped it to buyers who put it to work in their own environments. Often with assistance from the vendor or certified third parties, true, but the moving pieces of the industry owed a great deal to traditional manufacturing.

Today, things have changed. Many enterprise software vendors are still operating as they have for the past few decades, but pressure from competing models is mounting.

The distribution of software, of course, has changed dramatically. Physical media has for years been an anachronism, as it became much more efficient for buyer and seller to leverage digital distribution. But things hardly stopped there: from Salesforce.com’s 2004 IPO forward, mainstream customers began to assess more critically the costs and benefits of installing software on premises versus merely consuming it as a service. The company – whose product resembled traditional packaged application (CRM) with the exception of its delivery model – drew a bright line between its business and that of traditional vendors. Salesforce famously campaigned around a message of “No Software.” Its toll-free number, in fact, remains 1-800-NO-SOFTWARE. For some, this idea is comically inaccurate: without software, there is no Salesforce.com. It is still software, it’s just delivered via a different medium and managed by the vendor rather than the customer. For Salesforce, and presumably some subset of its customer base, however, the belief is that the distinction between SaaS and the traditional packaged software shipped to, installed on and managed from a customer’s premises is significant enough to render it a completely new product. A product, therefore, that should not be referred to as “software.”

Whatever one makes of the semantics of this argument, changes in the nature of software availability, delivery and procurement are clearly impacting markets and the incumbents who previously dominated them.

While Oracle may attribute its adjusted earnings miss this quarter to currency fluctuations, or its shortfall two quarters ago to a “lack of urgency” in its saleforce, the reality is that the trend line for its sales of new licenses has been problematic for well over a decade. Notably, this declining ability to sell new licenses of its software overlaps with rising adoption of open source software and SaaS packages, among other competitive models. This is no coincidence. While the underlying business and revenue models for open source and SaaS differ, they share one common advantage over traditional software distribution models such as Oracle: they are far easier to acquire.

Microsoft, another firm built largely on traditional software distribution and acquisition models, has similarly struggled to compete with more available alternatives. The company has telegraphed its level of concern with the viability of its traditional models moving forward with its massive investments in more available infrastructure (Azure), and this is appropriate. On the consumer front, Microsoft has seen Apple’s operating system distribution and pricing model shift from physical media priced at $200 to a free download. Within the server market, meanwhile, Microsoft’s biggest challenge of late has been competing in the rapidly growing (and inherently convenient) public cloud market where operating system licensing fees are near zero in most cases.

Microsoft and Oracle collectively generated billions of dollars of wealth according to the simple model described above: they manufactured software, shipped it to customers who were ultimately responsible for its installation, implementation, maintenance and usage. As barriers to hardware and software both have broken down, due to technical approaches such as open source, the public cloud or SaaS, the traditional model became increasingly subject to disruption. Adaptations from both have included the incorporation of the very models they were disrupted by: open source, public cloud and SaaS.

Absent substantial pressure, it’s unlikely that either of these businesses would have strayed from the courses that made them and their shareholders very wealthy. But selling software in the traditional manner became, and is becoming, more difficult to do.

Which brings us to the definitional question of what it means to be a “software” business. If companies as successful and well capitalized as Microsoft and Oracle are struggling with disruptions to traditional software distribution models, it would seem important for every software vendor to consider carefully what it means when it defines itself as a “software” vendor.

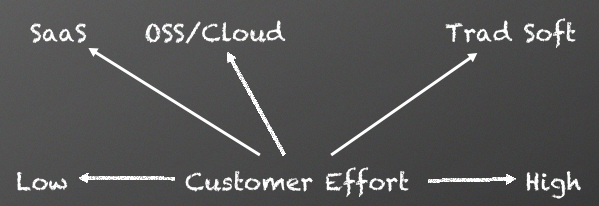

Given the market’s clear and accelerating preference for software models built on convenience – be that cloud, open source, SaaS or otherwise – it is useful for vendors and buyers alike to consider where a given product falls on a spectrum of customer effort.

-

At one end we have traditional software players, for whom procurement begins with on-site sales visits, nothing is free and access to the software is jealously guarded. From a customer perspective, this is a high effort model: the procurement process is time intensive, the costs of the software are high, and the customer typically bears the risk of implementation because they are paying for the software on an up front basis.

-

At the other end of the spectrum lies SaaS, which is accessible to anyone with a browser and payable via a credit card. The customer effort metric for SaaS is low: the software is comparatively easily acquired, so procurement is less involved, and implementation risk and effort is largely shifted to the vendor – for a longer term premium, of course.

-

Somewhere in between these models, but closer to the SaaS end of the spectrum, lie both open source software and public cloud services. Both are substantially advantaged versus traditional software and infrastructure in acquisition. Procurement is so low effort for customers, in fact, that both open source and public cloud services are frequently leveraged within organizations without technical leadership being aware of that fact. Because they do not represented a finished product, however, more implementation effort is required versus SaaS. Customer evaluation for public cloud and open source relative to SaaS – or PaaS, for that matter – is typically an evaluation of the tradeoffs between convenience and control.

Directionally, while there are obvious exceptions, from a macro perspective the market is actively shifting away from the traditional model towards the latter two examples. Which implies that vendor strategies must adapt to this changing reality; vendors whose model allows only for traditional models of software distribution and consumption will be at a significant disadvantage moving forward. Many, in fact, are already alarmingly behind. If a given software vendor isn’t at least considering strategic shifts in consumption and delivery of software in its market, it has a serious problem.

In a world in which the only option for customers is to purchase software up front and assemble and leverage it at their own risk, traditional software sales would remain robust, because software is a basic necessity. In today’s market context, however, where customers have a wealth of options, from purchasing, installing and running their own software stack to fully outsourcing same to constructing hybrid applications composed of micro-services (i.e. managed software exposed as an API), software vendors must cater to customer’s desires for convenience and effort minimization.

Even smaller software vendors must actively plan for a future in which they are not merely handing off a software product to customers and hoping for the best, but actively delivering it over a network, managing and monitoring it on behalf of customers in a public cloud, integrating data into the product and so on. This poses immense operational challenges, of course, as most pure software vendors are not appropriately resourced to deliver their software in a network context, for example. But if they don’t, they can be sure competitors will.

Vendors, whether that’s Cloudera or Pivotal as featured in the quote above, will continue to point to “software” as their primary revenue source. But the reality is that when successful companies say “software” they will actually mean software plus some combination of public cloud infrastructure, hardware/appliance, automated management/monitoring capabilities, hosted micro-services, and data enabled analytics. The majority of which is software, of course. Just not strictly software as we have been conditioned to think of it.

Which is why in a growing number of cases, the term “software company” may become as obsolete as the media they once distributed the product on.

Disclosure: Cloudera, Pivotal and Salesforce are current RedMonk customers. Microsoft has been a customer but is not currently, and neither Apple nor Oracle is a RedMonk customer.