If it seems odd to be posting predictions for the forthcoming year almost three months in, that’s because it is. In my defense, however, the 2015 iteration of this exercise comes little more than ten days late by last year’s standards. Which were, it must be said, very late themselves. Delayed or not, however, predictions are always a useful exercise if only, as Bryan Cantrill says, because they may tell us as much about the present as the future.

Before we continue, a brief introduction to how these predictions are formed, and the weight you may assign to them. The forecast here is based, variously, on both quantitative and qualitative assessments of products, projects and markets. For the sake of handicapping, the predictions are delivered in groups by probability; beginning with the most likely, concluding with the most volatile.

From the initial run in 2010, here is how my predictions have scored annually:

- 2010: 67%

- 2011: 82%

- 2012: 70%

- 2013: 55%

- 2014: 50%

You may note the steep downward trajectory in the success rate over the past four years. While rightly considered a reflection of my abilities as a forecaster, it is worth noting that the aggressiveness of the predictions was increased in the year 2013. This has led to possibly more interesting but provably less reliable predictions since; you may factor the adjustment in as you will.

Safe

- Amazon is Going to Become More Dominant Thanks to “Honeypots”

Very few today would argue that Amazon is anything other than the dominant player in the public cloud space. In spite of its substantial first mover advantage, the company has continued to execute at the frantic pace of a late market entrant. This has maintained or even extended the company’s lead, even as some of the largest technology companies in the world have realized their original mistake and scramble to throw resources at the market.In 2015, Amazon will become even more dominant thanks to its ability to land customers on what I term “honeypot” services – services that are exceedingly easy to consume, and thus attractive – and cross/upsell them to more difficult-to-replicate or proprietary AWS products. Which are, notably, higher margin. Examples of so-called “honeypot” services are basic compute (EC2) and storage (S3) services. As consumption of these services increases, which it is across a large number of customers and wide range of industries, the friction towards other AWS services such as Kinesis, Redshift and so on decreases and consumption goes up. Much as was the case with Microsoft’s Windows platform, the inertia to leave AWS will become excessive.

The logical question to ask about escalating consumption of services that are difficult or impossible to replicate outside of AWS, of course, is lock-in.

"if you decide to write your applications to the AWS API, congrats you have just replaced Larry Ellison with Jeff Bezos" @jmckenty

— Lawrence Crowther (@LozCrowther) February 22, 2015

The answer to what impact this will have on consumption can be found from examining the history of the software industry. If the experience of the past several decades, from IBM to Microsoft to VMware, tells us anything, it’s first that when asked directly, customers will deny any willingness to lock themselves into a single provider. It also demonstrates, however, that for the right value – be that cost, or more typically convenience or some combination of the two – they are almost universally willing to lock themselves into a single provider. Statements to the contrary notwithstanding. Convenience kills.

-

Kubernetes, Mesos, Spark et al are the New NoSQL

Not functionally, of course. But the chaos of the early NoSQL market is remarkably similar to the evolution of what we’re seeing from projects like Mesos or Spark. First, there has been a rapid introduction of a variety of products which require a new conceptual understanding of infrastructure to appreciate. Second, while there may be areas of overlap between projects, in general they are quite distinct from one another. Third, the market’s understanding of what these projects are for and how they are to be used is poor to quite poor.In the early days of NoSQL, for example, we used to regularly see queries to our content that were some variation of “hadoop vs mongodb vs redis.” While these projects all are similar in that they pertain to data, that is about all they have in common. This was not obvious to the market for some time, however, as generations accustomed to relational databases being the canonical means of persisting data struggled to adapt to a world of document and graph databases or MapReduce engines and key-value databases. In other words, the market took very dissimilar products and aggregated them all under the single category NoSQL, in spite of the fact that the majority of the products in said category were not comparable.

This is currently what we see when customers are evaluating projects like Kubernetes, Mesos and Spark: the initial investigation is less functional capability or performance than basic education. Not through any failing on the part of the individual projects, of course. It just takes time for markets to catch up. For 2015, then, expect these and similar projects to achieve higher levels of visibility, but remain poorly understood outside the technical elite.

If the term NoSQL was reintroduced in 2009 then, per Wikipedia, and may have achieved mainstream status in 2014, it may be 2020 before the orchestraters, schedulers and fabrics are household names.

Likely

- Docker will See Minimal Impact from Rocket

Following the announcement of CoreOS’s container runtime project, Rocket, we began to field a lot of questions about what this meant for Docker. Initially, of course, the answer was simply that it was too soon to say. As we’ve said many times, Docker is one of the fastest growing – in the visibility sense – projects we have ever seen. Along with Node.js and a few others, it piqued developer interest in a way and at a rate that is exceedingly rare. But past popularity, while strongly correlated with future popularity, is not a guarantee.In the time since, we’ve had a lot of conversations about Docker and Rocket, and the anecdotal evidence strongly suggested that the negative impact, if any, to Docker’s trajectory would be medium to long term. Most of the conversations we have had with people in and around the Docker ecosystem suggest that while they share some of CoreOS’s concerns (and have some not commonly cited), the project’s momentum was such that they were committed for the foreseeable future.

10+ weeks in, here's an updated look at activity in the core repos for Docker, Rocket, and LXD. pic.twitter.com/RAMFe8N1wr

— Donnie Berkholz (@dberkholz) January 20, 2015It’s still early, and the results are incomplete, but the quantitative data from my colleague above seems to support this conclusion. At least as measured by project activity, Docker’s trendline looks unimpacted by the announcement of Rocket. I expect this to continue in 2015. Note that this doesn’t mean that Rocket is without prospects: multiple third parties have told us they are open to the idea of supporting alternative container architectures. But in 2015, at least, Docker’s ascent should continue, if not necessarily at the same exponential rate.

-

Google Will Hedge its Bets with Java and Android, But Not Play the Swift Card

Languages and runtimes evolve, of course, and eventually Google may shift Android towards another language. Certainly the fledgling support for Go on the platform introduced in 1.4 was interesting, both because of the prospect of an alternative runtime option and because of the growth of Go itself.That being said, change is unlikely to be coming in 2015 if it arrives at all. For one, Go is a runtime largely focused on infrastructure for the time being. For another, Google has no real impetus to change at the moment. Undoubtedly the company is hedging its bets internally pending the outcome of “Oracle America, Inc. v. Google, Inc.,” which has seen the Supreme Court ask for the federal government’s opinions. And certainly the meteoric growth of Swift has to be comforting should the company need to make a clean break with Java.

But the bet here is, SCOTUS or no, we won’t see a major change on the Android platform in 2015.

-

Services Will Be the New Open Core

I’ve written extensively (for example) on how companies are continuing to shift away from the tried and true perpetual license model, and for those interested in this topic, I have an O’Reilly title on it due any day now entitled “The Software Paradox.” The question is what comes next?Looking at the industry today, it’s clear that at least with respect to infrastructure software, it is difficult to compete without some component of your solution – and typically, a core that is viable as a standalone product – being open source. As Cloudera co-founder Mike Olson puts it, “You can no longer win with a closed-source platform.” Which sounds like a win for open source, and indeed to some extent is.

It is equally true, however, that building an open source company is inherently more challenging than building one around proprietary software. This has led to the creation of a variety of complicated monetization mechanisms, which attempt to recreate proprietary margins while maintaining the spirit of the underlying open source project. Of these, open core has emerged as the most common. In this model, a company maintains an open source “core” while layering on premium, proprietary components.

While this model works reasonably well, it does create friction within the open source community, as the commercial organization is inevitably presented with complicated decisions to make about what to open source and what to withhold as proprietary software. Coupled with the fact that for some subset of users, the open source components may be “good enough” and it’s clear that while open core is a reasonable adaptation to the challenges of selling software today, it’s far from perfect.

Which is why we are and will continue to see companies turn to service-based revenue models as an alternative. When you’re selling a service instead of merely a product, many of the questions endemic to open core go away. And even in models where 100% of the source code is made available, selling services remains a simpler exercise because selling services is not just selling source code: it’s selling the ability to run, manage and maintain that code.

In the late 1990’s when the services model was first proposed by companies then referred to as “Application Service Providers,” the idea was laughable. Why rent when you could buy?

Whether it’s software or cars today, however, customers are increasingly turning towards on-demand, rental models. It’s partially an economic decision, as amortizing capex spend over a longer period of time in return for manageable premiums is often desirable. But more importantly, it’s about outsourcing everything from risk to construction, support and maintenance to third parties.

Consider, for example, Oracle. In the space of three years the company has gone from reporting on “New software licenses” in its SEC filings to “New software licenses,” “Cloud software-as-a-service and platform-as-a-service,” and “Cloud infrastructure-as-a-service.” There will be exceptions, as there always are, but the trajectory of this industry is clear and it’s towards services. We’ll leave the implications of this shift for open source as a topic for another day.

Possible

-

One Consumer IoT Provider is going to be Penetrated with Far Reaching Consequences

If it weren’t for the fact that there’s only ten months remaining in the year and the “far reaching” qualifier, this would be better categorized as “Likely” or even “Safe.” But really, this prediction is less about timing and more about inevitability. Given the near daily breaches of organizations regarded as technically capable, the longer the time horizon the closer the probability of a major IoT intrusion gets to 1. The attack surface of the consumer IoT market is expanding dramatically from thermostats to smoke detectors to alarms to light switches to door locks to security systems. Eventually one of these providers is going to be successfully attacked, and bad things will follow. The prediction here is that that happens this year, much as I hope otherwise. -

AWS Lambda Will be Cloned by Competitive Providers

With so many services already available and more being launched by the day, it’s difficult for any single service to stand out. Redshift is hailed as the fastest growing in the history of the BU, EC2 and S3 continue to provide the base core to build on, and accelerating strikes into application territory via WorkDocs and Workmail make it easy for newly launched AWS offerings to get lost. Particularly when they don’t fit pre-existing categories.For my money, however, Lambda was the most interesting service introduced by AWS last year. On the surface, it seems simplistic: little more than Node daemons, in fact. But as the industry moves towards services in general and microservices specifically, Lambda offers key advantages over competing models and will begin to push developer expectations. First, there’s no VM or instance overhead: Node snippets are hosted effectively in stasis, waiting on a particular trigger. Just as interest in lighter weight instances is driving containers, so too does it serve as incentive for Lambda adoption. Second, pricing is based on requests served – not running time. While the on-demand nature of the public cloud offered a truly pay-per-use model relative to traditional server deployments, Lambda pushes this model even further by redefining usage from merely running to actually executing. Third, Lambda not only enables but compels a services-based approach by lowering the friction and increasing the incentives towards the servicification of architectures.

Which is why I expect Lambda to be heavily influential if not cloned outright, and quickly.

Exciting

- Slack’s Next Valuation Will be Closer to WhatsApp than $1B

In late October of last year, Slack took $120M in new financing that valued the company at $1.12B. A few eyebrows were raised at that number: as Business Insider put it: “when it was given a $1.1 billion valuation last October, just 8 months after launching for the general public, there were some question marks surrounding its real value.”The prediction here, however, is that that number is going to seem hilariously light. The basic numbers are good. The company is adding $1M in ARR every 11 days, and has grown its user base by 33X in the past twelve months. Those users have sent 1.7B messages in that span.

But impressive as those numbers might be, how does that get Slack anywhere close to WhatsApp? The same month that Slack was valued at a billion dollars, WhatsApp hit 600 million users – or 1200 times what Slack is reporting today. How would they be even roughly comparable, then?

In part, because Slack’s users are likely to be more valuable than WhatsApp’s. The latter is free for users for the first year, then priced at $0.99 per annum following. Slack meanwhile, offers a free level of service with limitations on message retention, service integrations and so on, with paid pricing starting at $6.67 – per month. Premium packages go up to $12.50 per month, with enterprise services priced at $49-99 coming. This structure should allow Slack to hit a substantially higher ARPU than WhatsApp – which it will need to because it’s so far behind in subscriber count.

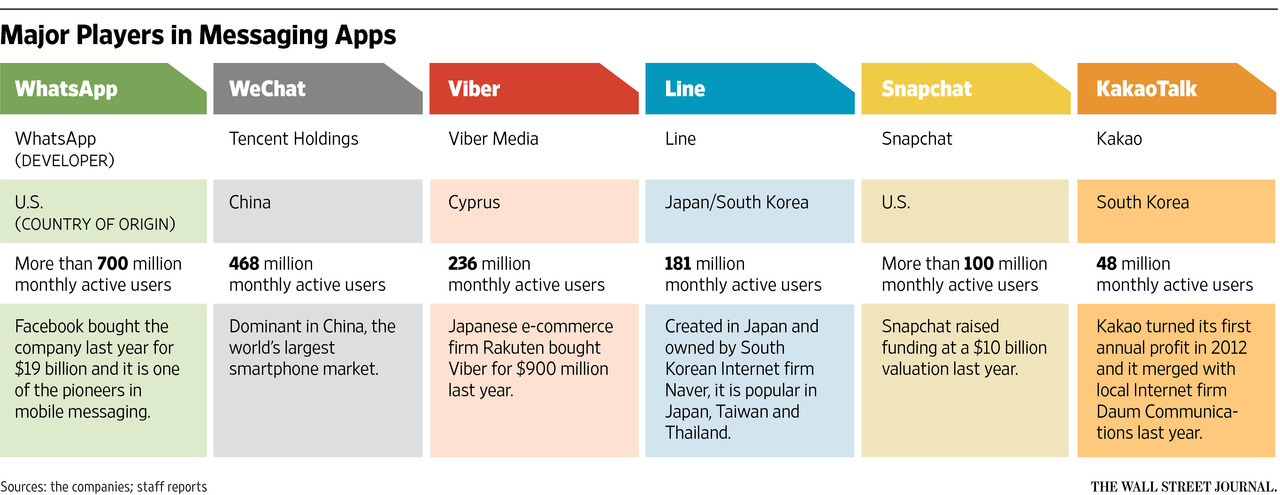

The real reason that Slack is undervalued, however, is because its versatility is currently being overlooked. Slack is currently viewed by parties external as a business messaging tool, not a consumer one. See, for example, this graphic from the Wall Street Journal.

Source: The Wall Street Journal

The omission of Slack here is understandable, because Slack itself has made no effort to brand itself or price itself as a consumer-friendly messaging tool. From the marketing to the revenue model, Slack is pitched as a product for teams.

The interesting thing, however, is that what makes it useful for teams also makes it useful for social groups. A group of my friends, for example, has turned Slack into a replacement not just for email or texting but WhatsApp. While a number of us started using WhatsApp while in Europe last year, Slack’s better for two reasons. First, it’s mobile capable, but not mobile only. True, WhatsApp has added web.whatsapp.com, but that’s Chrome only. And frankly, for a messaging app that you use heavily, a browser tab doesn’t offer the experience that a native app does – and Slack’s native apps are excellent. For Slack, the desktop is a first class citizen. For WhatsApp and the like, it’s an afterthought.

Second, the integrations model makes Slack far more than just a messaging platform. My particular group of friends has added a travel channel where our Foursquare and TripIt notifications are piped in, an Untappd channel where our various checkins are recorded, a blog channel which notifies us of posts by group members and so on. We also have our own Hubot linked to our Slack instance, so we can get anything from raccoon gifs to Simpsons quotes on demand.

Slack has been so successful with this group of friends, in fact, that I created another room for our local Portland chapter of Computers Anonymous. While it’s early, it seems as if the tool will have legs in terms of helping keep an otherwise highly distributed group of technologists in touch.

Anecdotal examples do not a valuation make, of course. And there’s no guarantee that Slack will do anything to advance this usage, or even continue to permit it. But it does speak to the company’s intrinsic ability to function well as a message platform outside of the target quote unquote business team model. What might a company with the ability to sell to both WhatsApp users and enterprises both be worth? My prediction for 2015 is a lot more than $1.12B.

Spectacular

-

The Apple Watch Will be the New Newton

If this were any other company besides Apple, this prediction would likely be in the “Safe” category. “Likely,” at worst. Smartwatches as currently conceived seem like solutions in search of a problem. Is anyone that desperate to see who’s calling them that they need a notification on their wrist? Who makes phone calls anymore anyway? As for social media and email notifications, aren’t we already dangerously interrupt driven enough? And then there’s the battery life. For the various Android flavors, it varies from poor to abysmal. Apple, for its part, hasn’t talked much about the battery life on their forthcoming device, which probably isn’t a great sign.But it’s Apple, and counting them out is dangerous business indeed. How many couldn’t see the point of combining a computer with a phone? Or the appeal of a tablet (in 2010, not 1993)? Hence the elevation of this prediction to the spectacular category.

It could very well be that Apple will find a real hook with the Watch and sell them hand over fist, but I’m predicting modest uptake – for Apple, anyway – in 2015. They’ll be popular in niches. The Apple faithful will find uses for it and ways to excuse the expected shortcomings of a first edition model. If John Gruber’s speculation on pricing is correct, meanwhile, Apple will sell a number of the gold plated Edition model to overly status conscious rich elites. But if recent rumors about battery life are even close to correct, I find it difficult to believe that the average iPhone user will be willing to charge his iPhone once a day and her watch twice in that span.

While betting against Apple has been a fool’s game for the better part of a decade, then, call me the fool. I’m betting the under on the Apple Watch. Smartwatches will get here eventually, I’m sure, but I don’t think the technology is quite here yet. Much as it wasn’t with the Newton once upon a time.

Donnie Berkholz says:

February 26, 2015 at 1:13 pm

My biggest concern with Slack in the non-business context you suggest is its inherently closed nature at present. I’d expect that to greatly impede discoverability and raise the barrier to new participants. That’s

fixable of course, but it’s unclear whether Slack would make the needed

changes.

stephen o'grady says:

February 26, 2015 at 4:31 pm

I agree, but there are signs Slack understands that:

https://twitter.com/llimllib/status/568202169301790720

Be interesting to see how it plays out.

Adam Seligman says:

February 26, 2015 at 11:38 pm

Love all the discussion of Services (with a capital S)

stephen o'grady says:

February 27, 2015 at 12:28 pm

I can see how you might

Three Short Links: March 2, 2015 - Apprenda says:

March 2, 2015 at 9:01 am

[…] What’s in Store for 2015 – Stephen O’Grady at Redmonk’s 2015 predictions. Always interesting, even if his success rate barely breaks 50% anymore. […]

bkkcanuck says:

March 7, 2015 at 4:04 pm

Google funds a number of open source projects. If I were them I would take some of that money and fund some technologies that could both disrupt Oracle v Java and provide an ecosystem for Android devices. It does not have to be swift, but it could be Scala — using that language as a starting point and building out both llvm and ovm (open vm / jvm replacement – which implements bytecode that is friendlier to multiple languages and paradigms). But instead of betting on one language, take the best of a few different paradigms and give developers options. Also build a few translation tools that help move from java. On the server side build there own database drivers that support fully parallel and non-blocking access to existing database and provide the tools for this to be used on the server side as well. Just start throwing wrenches at Oracle and seeing if something causes damage and frees people from their clutches (attacking their main business such as database would be foolhardy)